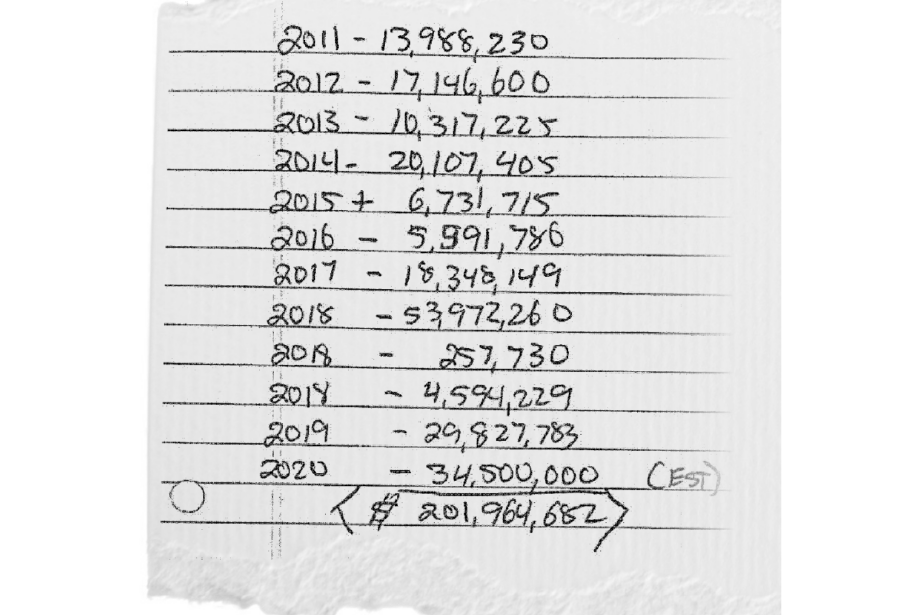

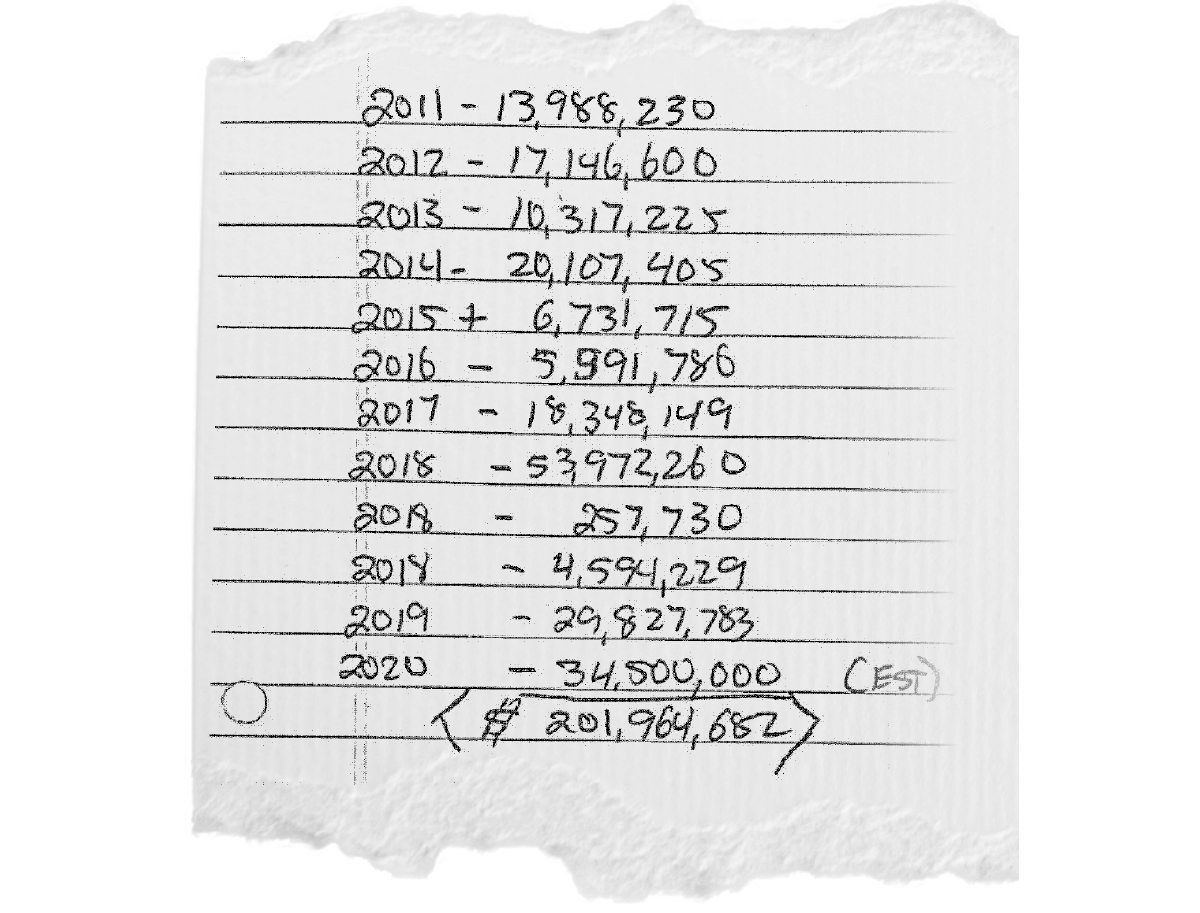

Cody Easterday provided Tyson Foods executives this handwritten document showing his losses from trading commodity futures contracts.

In a case of $233 million stolen by a Washington rancher who peddled nonexistent livestock, Tyson Foods Inc. of Springdale has learned you can’t see phantom cattle if you don’t look.

By the late fall of 2020, when subsidiary Tyson Fresh Meats Inc. began taking a closer look at its cattle investments, nearly a quarter billion dollars was out of the gate.

On Nov. 30, TFM of Dakota Dunes, South Dakota, made a shocking discovery: A cattle producer and feedlot operator it worked with for several years had confessed to submitting invoices for about 200,000 cattle that didn’t exist. The loss to Tyson and a Washington company topped $240 million, making it one of the largest fraud cases in recent memory.

Last month, Cody Allen Easterday, 49, of Mesa, Washington, pleaded guilty to one count of wire fraud and agreed to pay $233 million in restitution to Tyson and $11 million to the Washington company, which wasn’t named in the criminal file in U.S. District Court in Washington. Sentencing is set for August.

More: See the plea agreement and other court documents in the case.

Over several days starting Nov. 30, Easterday, an owner and former president of Easterday Ranches Inc. of Pasco, Washington, confessed to Tyson executives what he had done: He had used the stolen money dating back to 2016 to cover losses from trading commodity futures contracts. Between 2011 and 2020, those losses totaled $202 million.

“I was struck by Mr. Easterday’s demeanor during these meetings,” Kevin Hueser, TFM’s senior vice president for beef management, said in a Jan. 25 civil court filing. “While he did get a little teary-eyed at times, he was largely very straightforward and stoic. He did not show the remorse that I expected from someone who had defrauded our company out of hundreds of millions of dollars.”

A Washington bank also has alleged that Easterday Ranches owes tens of millions of dollars for defaulting on a loan taken out months before his confession.

In February, Easterday Ranches Inc. filed for Chapter 11 bankruptcy reorganization and listed $108.7 million in debts and $12.1 million in assets.

Hueser asked Easterday why he didn’t seek help from TFM years earlier. “He just replied that he probably should have done that, and that he had ‘screwed up,’” Hueser said. After the discovery, Tyson said in a Dec. 21 filing with the U.S. Securities & Exchange Commission that a supplier’s “misrepresentations” caused Tyson to overstate its live cattle inventory by about $285 million for its fiscal year that ended Oct. 3. Easterday wasn’t named in the filing, but Tyson said he represented about 2% of the total cattle supplied to its beef segment each fiscal year between 2017 and 2020. Tyson said it expected to amend its financial statements.

Gary Mickelson, a spokesman for Tyson, told Arkansas Business via email that the company is working with its “outside auditor to implement additional financial controls to help prevent or detect this type of activity in the future.”

But a law professor briefed on the situation said it was “baffling” that Tyson hadn’t done that sooner.

“I don’t know how long it takes to raise cattle to have them slaughtered, but at some point, auditors should go out and look and make sure there’s actually something there,” said Scott Schumacher of the University of Washington School of Law and a former attorney with the U.S. Department of Justice Tax Division.

“It’s just remarkable to me that they would spend that much money over a four-plus-year time frame” and never confirm the cattle were real, he said.

Neither Easterday nor his criminal defense attorney, Carl Oreskovich of Spokane, responded to requests for comment. But hundreds of pages of bankruptcy, civil and criminal court documents offer a look into Easterday’s crime.

In 1958, Easterday’s grandfather, Ervin Easterday, moved his family and farming operation from Idaho to southeastern Washington, according to the Easterday Farms’ website. The farm grew to more than 18,000 acres of potatoes, onions, corn and wheat, the website said.

In 1974, a related company, Easterday Ranches, was formed. And in 1979, Cody Easterday’s parents, Gale and Karen Easterday, became the sole owners of the operations.

Gale Easterday died on Dec. 10 at the age of 79. In a tribute to his father on Twitter, Cody Easterday shared an old family photo and wrote, “RIP you can always tell a man by the woman he decides to spend the rest of his life with. Here is my smoking hot mom Karen L Easterday at 23 years old with 2 of the 5 of us. What a life they lived from then until now.”

Gale A Easterday 3/13/41 to 12/10/20 RIP you can always tell a man by the woman he decides to spend the rest of his life with. Here is my smoking hot mom Karen L Easterday at 23 years old with 2 of the 5 of us. What a life they lived from then until now. Well done dad well done!! pic.twitter.com/JwpDtHBpRV

— Cody Easterday (@spudonioncattle) December 19, 2020

In 1989, Cody Easterday became a partner in Easterday Farms, which also filed for Chapter 11 bankruptcy protection in February. It listed $142.3 million in debts and $39.4 million in assets.

Bankruptcy filings show Easterday became a president of both Easterday companies in 1999. By 2010, Easterday Ranches had cattle feeding agreements that called for it to buy and fatten up cattle for delivery to TFM’s processing plant.

Easterday Ranches agreed to raise between 145,000 and 180,500 cattle annually for TFM, one of the largest beef processors in the United States. In its 2020 fiscal year, TFM had $15.8 billion in sales.

TFM covered all the cost of obtaining the cattle, feeding them and their care. When the cattle reached slaughter weight, TFM paid Easterday the market value of the cattle, minus the cost of securing and raising them. But if the market value didn’t cover the cost of raising the cattle, Easterday Ranches would owe TFM.

The court records don’t say when or why Easterday started speculative trading in the cattle futures market, but he used his personal trading accounts and Easterday Ranches’ corporate accounts.

The first known loss — $14 million — appeared in 2011, according to a handwritten document that Easterday showed Tyson executives. By the end of 2015, Easterday had losses totaling $54.8 million.

“The vast majority of those trading losses occurred in the corporate accounts,” according to a lawsuit filed March 31 by the Commodity Futures Trading Commission, the federal agency in charge of the administration and enforcement of the Commodity Exchange Act & Regulations.

“To cover margin calls, Easterday devised a scheme to defraud” TFM, the commission said in its suit, which is seeking restitution and penalties.

The Scheme

Easterday told Tyson executives that starting in 2016, as his commodities trading losses grew, he started submitting fake feeding invoices as well as the bogus cattle invoices to TFM, according to a statement by Jason Wenglarski, Tyson’s vice president of internal governance.

Easterday said proceeds from the fraudulent feeding statements were used to offset the feed costs for the real cattle he bought, and the sham invoices helped lower the profitability of the ghost cattle.

“Without feed cost included these cattle would have shown unusual profitability,” Wenglarski said. “The feed costs were added to allay any suspicions if Tyson noticed that the [fake] cattle were not being fed.”

For its fiscal year that ended Oct. 31, 2019, Easterday Ranches had $110.7 million in revenue, according to its bankruptcy filing. A year later, its revenue had fallen to $64.8 million.

Prior to his guilty plea, Easterday insisted that what he was doing was not stealing or fraud. “Rather he said he was overcharging Tyson on the front end and fully intended to pay Tyson back,” Wenglarski said.

Easterday told his office staff that he was “merely doing some ‘forward billing.’” But Wenglarski said Easterday never mentioned his self-approved billing arrangement to Tyson.

Wenglarski’s filing doesn’t say if Easterday gave a timeline for when he planned to repay TFM.

Meanwhile, Easterday’s trading losses were growing. In 2018 alone, his losses totaled $58.8 million. And by the end of last year, Easterday estimated he had lost a total of $202 million.

Easterday Ranches needed cash. On Aug. 20, Easterday Ranches borrowed $45 million from Washington Trust Bank of Spokane, according to a lawsuit the bank filed in January. Cody Easterday, his wife, Debby, and parents, Gale and Karen Easterday, personally guaranteed the loan. The bank said in the suit that Gale Easterday’s death in December and Tyson’s lawsuit triggered a default on the loan, and Easterday Ranches and the Easterdays owe the bank $44.8 million.

Discovery

In the fall of 2020, TFM’s Hueser received a report from accountants that TFM had about 286,000 head of cattle at Easterday Ranches, valued at about $320 million.

Hueser said that in the middle of November he spoke with Justin Nelson, TFM’s vice president for cattle procurement, about Easterday’s inventory. Hueser asked Nelson to confirm the location and number of Easterday’s cattle.

On the evening of Nov. 30, Nelson called Hueser at home with alarming news. “Justin told me that Mr. Easterday had confessed that he had submitted invoices to TFM for payments for cattle that did not actually exist,” Hueser said.

“That same evening, I alerted other TFM executives about this problem,” he said. “This began an intense week of meetings as we began to learn about the extent of this fraud and to develop plans for how to address it.”

The next morning, Easterday told Tyson executives that he owed TFM 200,000 head of cattle.

“I have been showing more cattle in inventory than I have on feed,” Easterday said during a call with executives, according to a statement filed in the case by Leah Andersen, TFM’s senior vice president of operations for finance and accounting.

Easterday also said that he didn’t have all the cattle that TFM paid for. “I violated your trust but that is where I am at,” Easterday said, according to Andersen.

He also assured the executives that Tyson’s supply chain was sound. “I have been delivering fat cattle and there is no jeopardy from a supply perspective,” Easterday said.

Easterday also showed executives how he “meticulously” kept track of both the cattle TFM paid for and the ghost cattle.

“He initially claimed that this scheme began in 2017,” Hueser said. “When we later confronted him with evidence that it actually began sometime in 2016, he agreed that was probably correct.”

Hueser asked Easterday what he did with the money he stole.

“He said he had lost all of the money on the futures market — specifically, he said he ‘had pissed it away on the Merc,’ a reference to the Chicago Mercantile Exchange,” Hueser said.

Easterday also defrauded the CME Group Inc., which operates the world’s largest financial derivatives exchange, according to a March 31 Department of Justice news release. On two separate occasions, Easterday submitted fake paperwork to the CME, resulting in Easterday Ranches being exempt from limits in live cattle futures contracts, the news release said.

Easterday stepped down as president of both Easterday Ranches and Easterday Farms on Jan. 29, days before the companies filed for bankruptcy protection.

About two months later, Easterday signed the criminal plea agreement.

Easterday’s sentencing is scheduled for Aug. 4 in U.S. District Court in the Eastern District of Washington. He faces up to 20 years in federal prison.