Automatically enrolling employees in their 401(k) plans, a trend that’s picking up around the United States, can help companies in several ways, according to employee benefits experts in Arkansas.

Automatic enrollment increases plan participation, and increased plan participation helps employers meet the “nondiscrimination” tests of the Internal Revenue Service. These tests seek to ensure that 401(k) plans, which come with tax breaks, are fair to all by determining whether contributions made by rank-and-file employees are proportional to contributions made by owners and managers — highly compensated employees, or HCEs, in IRS parlance.

The automatic enrollment strategy, in turn, helps companies recruit and retain high-value executives as well as rank-and-file employees.

In a traditional plan, rank-and-file participation matters because how much those employees contribute to a plan affects how much a company’s HCEs can defer into retirement accounts, according to CPA Phillip French of Frost PLLC in Little Rock. French is a third-party administrator of retirement plans sponsored by businesses.

HCEs are employees who made more than $120,000 in the current or previous year, owned at least 5 percent of the company they worked for or were in the top 20 percent of employees ranked by compensation at the company, according to the IRS.

The federal government increased the maximum amount an individual can contribute to a 401(k) to $18,500 in 2018. However, HCEs may not be allowed to contribute that maximum, Alexandra Ifrah told Arkansas Business. Ifrah is a partner in the Employee Benefits Practice Group of Friday Eldredge & Clark in Little Rock.

HCEs can’t contribute the maximum if their company doesn’t get sufficient rank-and-file participation for their contributions to pass the nondiscrimination tests, she said.

French and Ifrah join the IRS in emphasizing that automatic enrollment helps 401(k) plans pass the tests.

Automatic Enrollment Rises

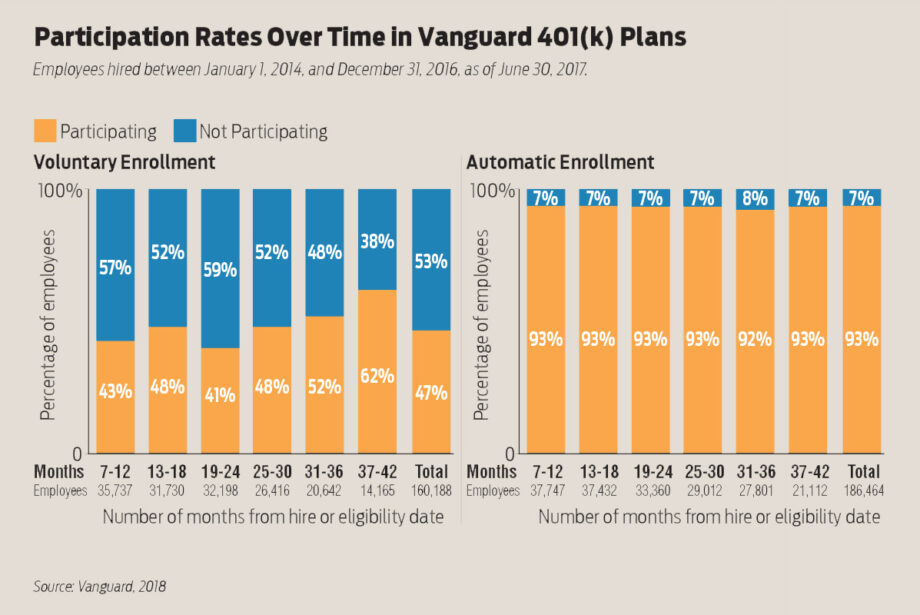

Automatic enrollment has become more prevalent since the Pension Protection Act of 2006 clarified that employers could withhold wages for that specific purpose without employees opting into their 401(k) plan first.

Sixty-eight percent of companies automatically enroll workers in 401(k) plans, up from 58 percent in 2015, according to Alight Solutions’ 2017 survey of 333 large U.S. employers. Alight Solutions, of Lincolnshire, Illinois, is a provider of benefits administration and cloud-based human resources and financial services.

“Here’s kind of how it works: People do not like to make decisions, so if the decision is made for them, they tend to go with it,” French said.

Most of the workers employed by one of French’s clients, Advanced Cabling Systems of North Little Rock, have done just that. The company implemented automatic enrollment within the past year, and participation in its plan has “gone up tremendously,” Human Resources Manager Holly Hall said.

The company has 178 employees; 157 of them are enrolled in its traditional 401(k) plan.

Hall said Advanced Cabling implemented automatic enrollment because enrollment forms were getting overlooked amid all the other paperwork new hires receive, and that meant that its employees might not be saving for retirement.

Now their 401(k) plan provider, Voya Financial, mails new hires a packet that informs them that they will be automatically enrolled in the company’s 401(k) plan at a 3 percent deferral rate. That means 3 percent of each employee’s gross salary will be taken out of every paycheck, pre-tax, and placed into that employee’s retirement account.

Advanced Cabling also offers a guaranteed match to its employees. Hall said the company matches up to 6 percent of an employee’s gross salary. If an employee defers 3 percent, then he gets a 3 percent match. If he defers 6 percent or more, he gets a 6 percent match.

The match is dollar-to-dollar and week-by-week, Hall added. It’s not awarded at the end of the year, as is the case with most plans, and employees can see the employer match on every paycheck stub.

Voya also has a mobile app that allows employees to quickly and easily change their deferral rate, access their account information and adjust their investments at any time, without filling out paperwork.

Having automatic enrollment “really goes a long way with the employees because they know that you have their best interests at heart, that you are looking at them as people and not just as a number,” Hall said.

Although the company isn’t benefiting financially from the practice because it is paying out more in matches due to increased participation, its benefits inspire loyalty from employees and contribute to recruiting and retention, she said.

Auto enrollment has worked well for Advanced Cabling, but it isn’t always the right option for a company; the practice does have “cons” as well as “pros.”

“That’s probably the biggest ‘con,’ right there, is if the plan has a match, your cost is going to go up because your deferrals are going to go up,” French said.

“I guess there would always be a few people, I haven’t seen it, but I would suspect there’s going to be some people who are upset when one day they wake up and see their paycheck is diminished and they don’t know why because they didn’t read the notice and weren’t staying informed and all that,” he said. “Then, I guess, the other con is it’s just one more hoop you have to step through as an employer to keep your plan in compliance.”

Companies with high turnover that implement auto enrollment could end up with a lot of small account balances, Ifrah added.

It also doesn’t make sense for very small companies like doctors’ offices and law firms to implement auto enrollment, the attorney said. Those are unlikely to pass the IRS tests either way and will likely need a safe harbor plan where rank-and-file participation and contributions don’t affect how much highly paid workers and owners can contribute to their 401(k) accounts.